Futures Market: Overnight, LME copper opened at $9,358/mt, fluctuated rangebound initially, then dipped to $9,315/mt. It fluctuated upward during the session, reaching $9,366/mt near the close, and finally settled at $9,356.5/mt, down 1.02%. Trading volume reached 18,000 lots, and open interest stood at 288,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 76,750 yuan/mt, dipped to 76,530 yuan/mt initially, consolidated during the session, and fluctuated rangebound near the close, reaching 76,860 yuan/mt before settling at 76,780 yuan/mt, down 0.65%. Trading volume reached 30,000 lots, and open interest stood at 178,000 lots.

【SMM Copper Morning Briefing】News: (1) Fed Chairman Jerome Powell attended the Senate Banking, Housing, and Urban Affairs Committee hearing. Powell reiterated that there is no urgency to adjust interest rates. The Fed's framework review will not include a focus on the inflation target, which will remain at 2%. (2) The Copper Industry High-Quality Development Implementation Plan (2025-2027) stated that by 2027, the resilience and security level of the industry chain and supply chain will be significantly improved. Copper raw material supply capacity will be continuously enhanced, aiming for a 5%-10% increase in domestic copper ore resources, and the recycling and utilization level of secondary copper will be further improved.

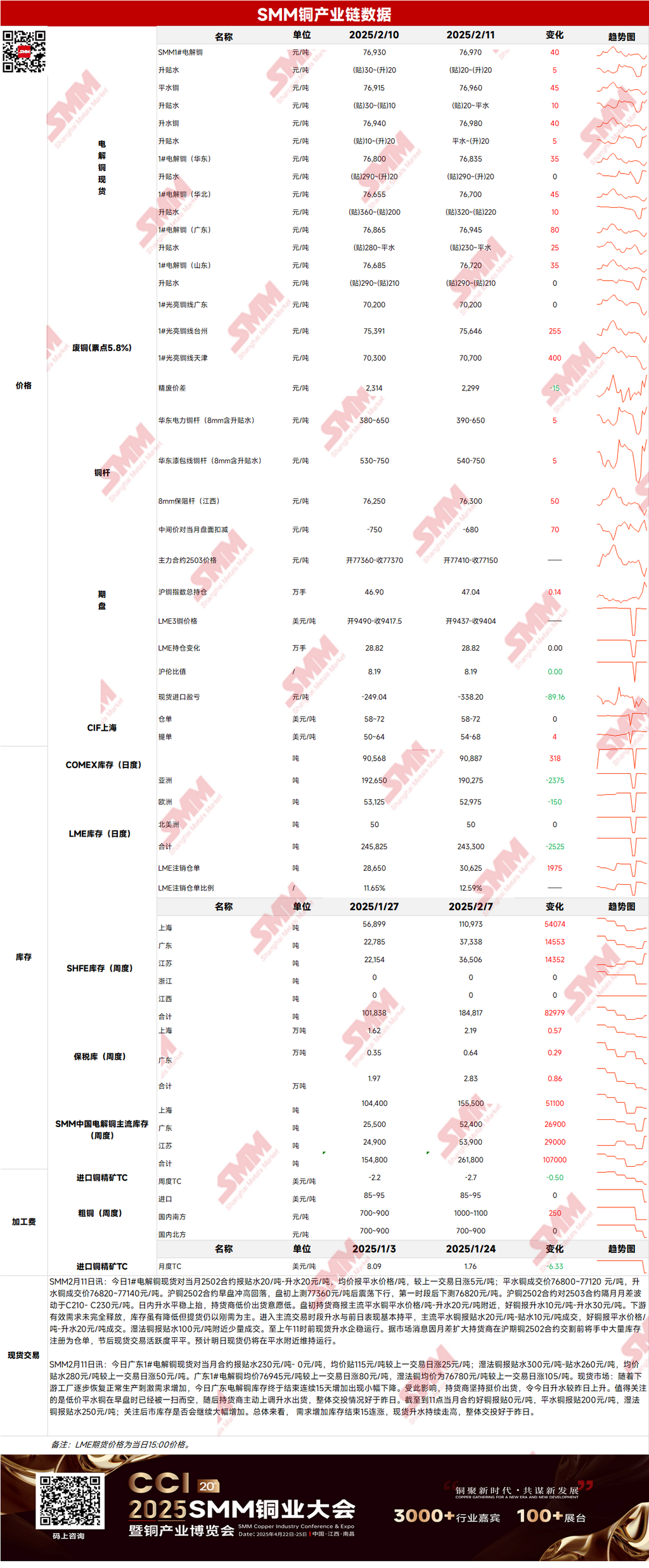

Spot Market: (1) Shanghai: On February 11, #1 copper cathode spot prices against the front-month 2502 contract were quoted at a discount of 20 yuan/mt to a premium of 20 yuan/mt, with an average price at parity. This was up 5 yuan/mt MoM. According to market sources, due to the widening price spread between futures contracts, suppliers registered a large amount of inventory as SHFE warrants before the delivery of the SHFE copper 2502 contract. Post-holiday spot trading activity remained subdued. Spot prices are expected to remain around parity today.

(2) Guangdong: On February 11, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 230 yuan/mt to parity, with an average price at a discount of 115 yuan/mt, up 25 yuan/mt MoM. Overall, demand increased, and inventory ended a 15-day consecutive rise. Spot premiums continued to climb, and overall trading was better than the previous day.

(3) Imported Copper: On February 11, warehouse warrant prices ranged from $58 to $72/mt (QP February), with the average price unchanged MoM. B/L prices ranged from $54 to $68/mt (QP March), with the average price up $4/mt MoM. EQ copper (CIF B/L) prices ranged from $4/mt to $18/mt (QP March), with the average price up $1/mt MoM. Quotes referenced cargoes arriving in late February and early March. The SHFE/LME price ratio weakened yesterday, and market offers were relatively quiet. However, demand for mid-to-late February and March cargoes remained high, especially for registered pyrometallurgical B/Ls. Buyers and sellers had significant differences, leading to a polarized market.

(4) Secondary Copper: On February 11, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 70,100-70,300 yuan/mt, unchanged from the previous trading day. The price difference between primary metal and scrap was 2,299 yuan/mt, down 15 yuan/mt MoM. The price difference for secondary copper rods was 1,200 yuan/mt. According to the SMM survey, post-holiday copper prices rose by 2,000 yuan/mt. Many secondary copper rod enterprises reported no significant difficulty in procurement, while suppliers, concerned about potential price drops for subsequent inventory, were more willing to sell.

(5) Inventory: On February 11, LME copper cathode inventory decreased by 2,525 mt to 243,300 mt. On the same day, SHFE warrant inventory increased by 12,099 mt to 80,303 mt.

Prices: Macro side, in his opening remarks at the Senate Banking Committee hearing, Powell stated that given the "overall strength" of the economy, low unemployment, and inflation still above the Fed's 2% target, the Fed is not in a hurry to lower short-term interest rates again, leading to a decline in copper prices. The market is also awaiting more details on potential trade tariffs from Trump. Fundamentals side, according to market sources, due to the widening price spread between futures contracts, suppliers registered a large amount of inventory as SHFE warrants before the delivery of the SHFE copper 2502 contract. Downstream demand has not fully recovered, and although inventory has decreased, cargo pick-up remains demand-driven. Post-holiday spot trading activity remained subdued. In terms of prices, the market is largely in a wait-and-see mode. The US January CPI data will be released today, and copper prices are expected to stabilize.

》Click to View the SMM Metal Database

【The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided herein is for reference only. This article does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】

![Copper Prices and Inventories Both Declined, Suppliers Actively Held Prices Firm and Made Shipments [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/vdbfy20251217171709.jpg)